Environmental Taxes Bulletin commentary (June 2021)

Published 30 June 2021

© Crown copyright 2021

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/statistics/environmental-taxes-bulletin/environmental-taxes-bulletin-commentary-june-2021

Headlines

Total provisional Climate Change Levy (CCL) and Carbon Price Floor (CPF) receipts for the last complete financial year 2020 to 2021 were £1,745 million, which is £259 million (12.9%) lower than the previous financial year.

Total provisional Landfill Tax (LFT) receipts for the last complete financial year 2020 to 2021 were £566 million, which is £75 million (11.7%) lower than the previous financial year.

Total provisional Aggregates Levy (AGL) receipts for the last complete financial year 2020 to 2021 were £359 million, which is £38 million (9.5%) lower than the previous financial year.

About this release

This bulletin is newly created for June 2021 and will be updated annually every June. The content was previously published in three separate bulletins, and was created following a consultation on the reduction and consolidation of HMRC statistics publications.

HMRC welcomes user engagement to improve the department’s National and Official Statistics. You can contact statistics producers on GOV.UK or the team responsible for this bulletin directly at revenuemonitoring@hmrc.gov.uk.

This publication provides statistics for:

- CCL and CPF

- LFT

- AGL

The latest release has been updated with provisional receipts data from October 2020 to May 2021 and provisional declarations data from September 2020 to April 2021.

Difficulties faced by taxpayers submitting returns during the coronavirus pandemic also means these statistics should be treated with additional caution in the financial year ending in 2021.

The ‘Environmental Taxes Bulletin’ is Crown Copyright. The information contained can be used as long as the source is made clear by the user.

Historical trends in environmental tax receipts over the past 10 years

Figure 1: Total environmental tax receipts for the previous 10 financial years, in £million

Figure 1 demonstrates the following trends:

- CPF was introduced on the 1 April 2013, which added a new rate for fossil fuels used to generate electricity, consequently, there was a substantial increase in CCL and CPF receipts from the financial year ending in 2013, since the financial year ending in 2015, CCL and CPF has been the largest environmental tax

- LFT was the largest environmental tax until the financial year ending in 2015, in the last 10 financial years it has largely decreased year on year from the financial year ending in 2014 through to the financial year ending in 2021, standard rate LFT charged has increased substantially in this period

- AGL receipts have been the smallest of the three environmental taxes for the past 10 financial years, receipts generally increased from the financial year ending in 2013 until the financial year ending in 2020, in the last financial year receipts have dropped from this peak

Table 1: Financial year environmental tax receipts for the previous 10 complete financial years, £ million

| Financial Year | CCL and CPF | LFT | AGL |

|---|---|---|---|

| 2011 to 2012 | 675.5 | 1,089.5 | 290.4 |

| 2012 to 2013 | 635.4 | 1,091.9 | 265.1 |

| 2013 to 2014 | 1,068.5 | 1,189.4 | 284.6 |

| 2014 to 2015 | 1,491.1 | 1,144.4 | 341.5 |

| 2015 to 2016 | 1,762.7 | 919.3 | 356.2 |

| 2016 to 2017 | 1,864.0 | 873.8 | 374.4 |

| 2017 to 2018 | 1,861.2 | 757.2 | 376.4 |

| 2018 to 2019 | 1,922.3 | 682.7 | 367.4 |

| 2019 to 2020 | 2,004.0 | 640.8 | 396.9 |

| 2020 to 2021 | 1,744.9 | 566.1 | 359.2 |

Climate Change Levy and Carbon Price Floor receipts and declarations

CCL is chargeable on the industrial and commercial supply of taxable commodities for lighting, heating and power by consumers in the following sectors:

- industry

- commerce

- agriculture

- public administration

- other services

CCL does not apply to taxable commodities used by domestic consumers or charities for non-business use.

CCL is charged on taxable supplies. Taxable supplies are certain supplies of the following taxable commodities:

- electricity

- natural gas as supplied by a gas utility

- petroleum and hydrocarbon gas in a liquid state

- coal and lignite

- coke and semi coke of coal or lignite

- petroleum coke

CPF is a tax on fossil fuels used in the generation of electricity. It was achieved through changes to the existing CCL regime for gas, solid fuels and liquefied petroleum gas (LPG) used for electricity generation. These changes included the introduction of new carbon price support (CPS) rates of CCL.

This publication provides Official Statistics for CCL and CPF receipts and declarations by fuel type:

- electricity

- gas

- solid and other fuels, including liquefied petroleum gas (LPG)

It is not possible to provide accurate separate receipts statistics for CCL and CPF because taxpayers pay receipts for both as one payment. An estimate of separate receipts statistics for CCL and CPF is provided using taxpayer returns data and should be treated with caution.

CCL and CPF taxpayers mainly follow quarterly accounting periods. Tax returns are due by the end of the month following the accounting period. Payment of tax is also generally due to HMRC by the same time, but taxpayers who pay by direct debit are given a 7 day extension.

These accounting periods and payment patterns cause a 1 to 2 month lag between accounting periods ending and receipts being received by HMRC.

Quarterly totals provide more meaningful comparisons because of this quarterly stagger pattern.

Figure 2: Total CCL and CPF receipts by financial year, in £million

Figure 2 demonstrates the following trends for total CCL and CPF receipts:

- CCL and CPF receipts have fallen in the financial year ending in 2021, potentially due to impacts from the government’s response to the Coronavirus (COVID-19) pandemic, as national lockdown policies most likely reduced the demand for energy amongst commodities covered by CCL and CPF

- CCL and CPF receipts peaked in the financial year ending in 2020 at £2,004 million, this grew from £635 million in the financial year ending 2013

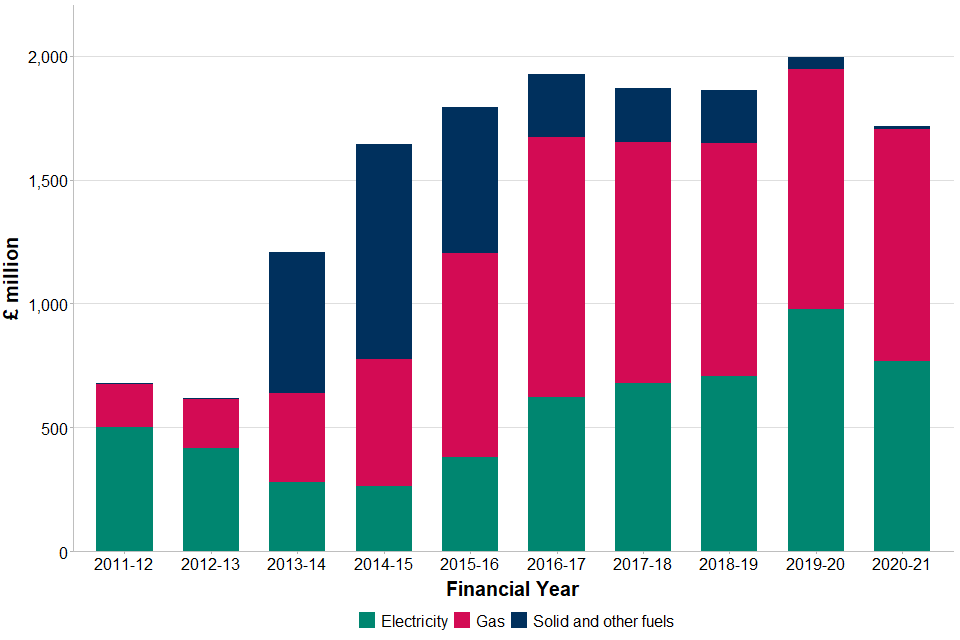

Figure 3: Total CCL and CPF declarations split by electricity, gas, and solid and other fuels by financial year, in £million

Figure 3 demonstrates several trends for total CCL and CPF declarations:

- CCL and CPF declarations have increased substantially in the last 10 financial years, this has mainly been driven through increasing gas declarations between the financial years ending in 2014 and 2017, and then increasing electricity declarations between the financial years ending in 2015 to 2020

- declarations for solid and other fuels have followed a consistent downward trend, likely reflecting declining quantities of coal used for electricity production in the UK

- the provisional 2020 to 2021 financial year (April to March) total for CCL and CPF declarations is £1,715 million, which is £267 million (13.5%) lower than the previous financial year

Landfill Tax receipts and declarations

LFT is a tax paid by landfill operators on the disposal of material at a landfill site. The tax is passed onto businesses and local authorities through the gate fee for disposing of waste at a landfill.

The tax aims to provide incentive for the diversion of waste from landfill to other less harmful methods of waste management such as recycling and incineration.

The tax is charged by weight. There are two rates; standard rate and lower rate.

- lower rate applies to non-hazardous and less polluting materials

- standard rate applies to all other taxable materials including all disposals at an unauthorised site

With effect from 1 April 2021, the following rates apply:

- lower rate: £3.10 per tonne

- standard rate: £96.70 per tonne

Exemptions exist for dredging, mining and quarrying waste, pet cemeteries, filling of quarries and waste from visiting forces.

Figure 4: Total LFT receipts by financial year, in £million

Figure 4 demonstrates the following trends for LFT receipts:

- LFT receipts have fallen substantially in the last 10 financial years, in the financial year ending 2014 they stood at £1,189 million, by the most recent financial year ending in 2021, they had fallen to £566 million

- LFT rates have increased year on year over the past 10 years, demonstrated through the change for standard rate charged which increased from £56.00 to £96.70 a tonne between 2011 and 2021, but LFT receipts have fallen since the financial year ending in 2014

- a ‘shortfall’ in LFT receipts should not necessarily be considered as a concern because the tax aims to provide incentive for the diversion of waste from landfill to other less harmful methods of waste management such as recycling and incineration, this turn away from standard rated waste can be seen below in the declarations data

Figure 5: Total LFT tonnage declared split by taxable tonnage, taxable tonnage of which relieved and exempt tonnage by financial year, in millions of tonnes

Figure 5 demonstrates several trends for LFT tonnage:

- standard rate tonnage has shown a steep downwards trend over the last 10 years in both number and proportion of LFT declarations

- lower rate tonnage has shown a modest downwards trend in numbers over the last 10 years but has increased as a proportion of LFT declarations due to falling standard rate tonnage

- exempt tonnage has shown greater fluctuation with a downwards trend over the last 10 years, as a proportion of LFT it has peaked at around 29% of LFT declarations in the financial year ending in 2019 but has lowered since then

- total tonnage has shown a downwards trend over the last 10 years

- the provisional 2020 to 2021 financial year (April to March) total for LFT tonnage declared is 20 million tonnes, which is 3 million tonnes (12.1%) lower than the previous financial year

Aggregates Levy receipts and declarations

This publication provides Official Statistics on AGL receipts and declarations.

AGL covers digging, dredging or importing aggregate commercially in the UK.

The current rate is £2 per tonne.

Traders become liable for the levy when an aggregate is:

- used for construction purposes

- mixed with anything other than water (excluding special circumstances)

- removed from:

- its originating site

- a connected site which is registered under the same name as the originating site

- a site where it had been intended to apply an exempt process to it, but this process was not applied

Total AGL tonnage declared is calculated by summing taxable and exempt tonnage declared (relieved tonnage is excluded from the calculation in order to avoid double counting as it’s contained within taxable tonnage). As taxable tonnage forms the majority of the total tonnage declared, the pattern of total tonnage is dominated by patterns in taxable tonnage.

Figure 6: Total AGL receipts by financial year, in £million

Figure 6 demonstrates several trends for AGL tonnage receipts:

- AGL receipts have generally risen over the last 10 financial years, in the financial year ending in 2012 AGL receipts stood at £290 million, by the financial year ending in 2021 AGL receipts were £359 million

- AGL receipts have a degree of fluctuation, receipts increased from the financial year ending in 2013 until the financial year ending in 2020 (with a small drop in 2018 to 2019), in the last financial year receipts have dropped from this peak

Figure 7: Total AGL tonnage declared split by taxable tonnage, taxable tonnage of which relieved and exempt tonnage by financial year, in millions of tonnes

Figure 7 demonstrates several trends for AGL tonnage declarations:

- taxable AGL declarations had increased year on year between the financial years ending in 2012 and 2020 (except in 2017 to 2018), the proportion of taxable tonnage has remained at 83% of AGL declarations for the past 5 years

- the provisional 2020 to 2021 financial year (April to March) total for AGL tonnage declared is 229 million tonnes, which is 22 million tonnes (8.8%) lower than the previous financial year